Those that know me well will confirm that I like to make a list or two. I find nothing better than to outline clear tasks and priorities and, more importantly, make sure I don’t forget anything! In the spirit of list making, I thought it would be good to share some key ways to save for retirement. In my experience as a Wealth Planner, I regularly come across people seeking my advice because they are concerned that they have not saved enough to allow them to retire comfortably. In fact, many admit they are expecting to be in debt once they finish working.

To help ensure you are doing enough to build up a sufficient retirement pot, here are my top tips. I hope that you can already tick these as completed; however, if you would like some advice please get in touch.

1. Join your company pension scheme

With new government legislation in place, all employers must have a pension scheme and be contributing at least 3% of salary for their employees, by April 2019. Most large companies have already set up their schemes, and for you to be receiving a pension contribution from your employer is a valuable additional benefit, even if you already have a personal pension in place.

It’s free money, so ensure you are in the scheme!

2. Do not delay

Simply put, the sooner you begin saving, the healthier your retirement pot will look. There is a greater benefit to starting to save as early as you can rather than just putting more in the pot; this is due to the effect of ‘compound growth’.

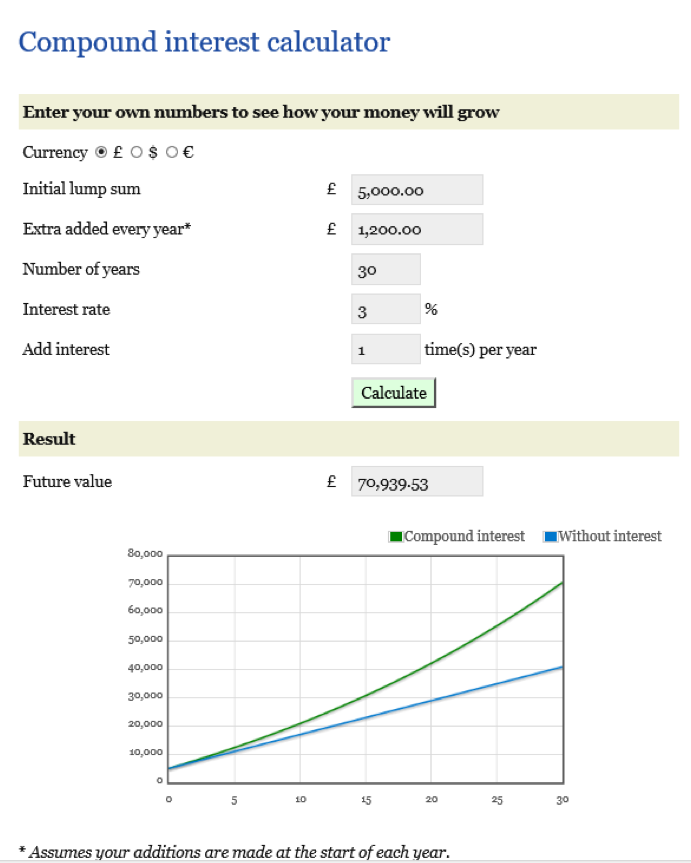

Click to view full-size

Taking a simple example, you can see the dramatic effect that compound growth can have over time in the example on the right.

You can see that the effect of receiving compound growth (growth on growth) over 30 years could nearly double your money.

[Past performance does not in any way guarantee future returns and the value of units held in all funds can fall as well as rise. It is possible that your investment could lose money, especially over the short term and you must be prepared to accept this risk].

3. Pensions have tax benefits – have you claimed all yours?

Investing in a pension can provide significant tax advantages, even when compared to savings accounts, ISAs or other types of investments. The government wants us to save for retirement, so the money we save into a pension receives ‘tax relief’.

As a basic rate taxpayer, most schemes will take your contribution after you have already paid basic rate income tax at 20%. The pension provider will then increase your contribution automatically by 20% and you will receive the tax relief straight into your pension plan.

As a high or additional rate tax payer (if you have income of over £43,000 in 2016/17 tax year), you pay 40 or 45% tax. Your pension contributions attract tax relief ‘at your highest rate’ and therefore, if the pension provider only gives you 20% tax relief, you are due a further 20 or 25% back via the Inland Revenue. Many people over the years have fallen into the trap of not claiming back this additional tax relief. You just need to tell the Inland Revenue how much you pay into a pension each tax year either by the self-assessment process or by calling them direct. The Inland Revenue will either send you a cheque or adjust your tax band accordingly for the next year.

If you have not done this before you are able to make a historical claim over a maximum of four years. I have managed to claim back thousands of pounds for clients in this way; the largest rebate for one client was £8000.

4. Do not amalgamate plans just to reduce paperwork

Over the years we all build up a number of pension pots from different employers, time being self-employed, or even periods when you could ‘contract out of the state pension’. Many clients first reaction is to try to amalgamate all their plans to reduce the amount of ongoing paperwork sent to them.

Although I understand the paperwork can be a bit annoying, you could stand to lose valuable benefits if you do not investigate the fine print before you amalgamate. Some pensions, particularly the older style ones, do have benefits or options that the new style plans cannot offer, such as additional life assurance, guaranteed growth rates, or additional tax-free cash.

However, sometimes it can be beneficial to amalgamate plans, particularly if some of your plans have high charges and no added benefits. Make sure you seek professional financial advice before moving pensions, to ensure you are doing the best thing. Once they are transferred you cannot change your mind.

5. Charges – do you know what you are paying?

The effect of ongoing charges to your pension or underlying investment can have the opposite effect of compound interest (see point 2).

Over the years, charges can have a negative effect on your pension fund and many clients do not know if the charges on their plans are competitive or if they are over the odds. An independent review can help you understand and evaluate the charges being taken from your plan. Read more about the effects fees can have on your pension in Andrew Pereira’s post ‘Compounding – Why 1% Matters’.

6. Attend regular pension reviews

Whether you have your own financial advisor, your work offers access to one, or you manage your pensions yourself, you need to keep up to date with the values of your plans, the underlying investment performance, and risk you are taking.

Research shows that half of the population aged over 50 do not know the value of their pensions, which is a seriously concerning statistic. I find most people become more interested in their pensions later in life. However, if you start good habits early it can really help you understand your financial position in retirement.

7. Keep up to date with State Pension provision

I class the state pension as a ‘top up’ to your private pension provision, but it is an important part of your overall retirement plan.

Many people make the mistake of thinking they can rely on the state pension alone. Currently, the basic state pension is £119.30 per week, or £155.65 per week if you reach state pension age after April 2016 and hence are eligible for the ‘new’ state pension. Clearly, neither of these figures are enough to retire on.

The state pension has changed dramatically over the last few years and keeping informed of these changes is imperative. For further details, read Andy Hearne’s post ‘The State Pension is Changing’.

8. Do not rely on selling your home or inheritance promises

Many people, when planning for retirement, consider downsizing their home and realising some of their assets from their property, to top up their income.

The reality is, however, that when it actually comes to retirement, most people would like to stay in their current home, so that they can spend their new found leisure time in an area they know and with friends and family who are close by.

To be able to downsize and realise enough funds to generally make the move effective, clients often have to move to a completely different area. While this works for some, it would be nice for this to be a ‘choice’ rather than a ‘necessity’.

In addition to realising assets from their property, many rely on the prospect of receiving an inheritance to top up their future savings. Again, it would be far better to consider this as a ‘nice to have’, rather than a core part of your retirement planning.

9. Keep up to date with pension legislation

Pension legislation has changed dramatically and is likely to continue to change in years to come.

The age at which you can access a pension fund, the amount you can put into your pension, and how you actually access the pot in retirement have all changed over the past ten to fifteen years.

One of my worst experiences as an Adviser occurred during a meeting with a client who had not taken any pensions advice since he set up his plan 30 years before. He had just celebrated his 50th birthday and was getting ready to retire and access his pension pot. Little did he know that a number of years previously the rules had changed and the age he could access his pension had increased from age 50 to age 55! As you can imagine, he was not very happy to say the least!

Keeping up to date with major changes to legislation is imperative to ensure your plans are on track. Learn more by reading Dominic Lobo’s post ‘HMRC Promised to Simplify Pensions’.

10. All is not lost!

Over the years we change jobs, move house and lose paperwork. It may even be that you are not sure of exactly what pensions you own and where they are held.

All pensions are linked to your National Insurance number and if you think you may have lost vital pension information, the ‘Pension Tracing Service’ may be able to help: https://www.gov.uk/find-pension-contact-details.

Pension Tracing Service

Telephone: 0345 6002 537

From outside the UK: +44 (0)191 215 4491

Textphone: 0345 3000 169

Monday to Friday, 8am to 6pm

If you can follow or maybe have already actioned some of my tips to save for retirement, you may well be in a better position to enjoy the life you have ahead of you.

—

This article does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs. Past performance is not a guide to future performance. The value of an investment and the income from it may go down as well as up and investors may not get back the amount originally invested. This document may include forward-looking statements that are based upon our current opinions, expectations and projections.