After months of speculation – and plenty of drama in between – we now know that Donald Trump will be returning to the White House in January 2025. At the time of writing, he has secured well over the 270 electoral college votes required to win the election, and with that he becomes only the second non-consecutive two-term President in US history.

Whether or not he has full control of Congress too, with a full sweep of both the Senate (already won) and House (votes still being counted) remains to be seen, and this will dictate the boundaries of power under the next Trump administration.

What does this mean for markets?

Investors will now pore over the details of what a second Trump term may look like – including focus on his trade policies, fiscal expenditure and potential squeeze on labour supply – all of which is understandable. We have already seen plenty of upward movement across US smaller companies, which stand to benefit from Trump’s more protectionist agenda, whilst other assets such as financials and oil and gas companies have also done well overnight, in the immediate aftermath of the result.

By contrast, because of concerns around higher level of government expenditure and less revenue coming in due to a lower tax regime, bond markets in the US had already begun to price this in pre-election, and this only manifested itself further as the result became clearer. With 10yr yields in the US now higher at 4.46% (a function of lower prices), this reflects some concern around Trump’s fiscal discipline.

Tuning out the noise

However, whilst the next few weeks will likely see plenty of ‘noise’ in the markets, as investors look to interpret his picks for the newly formed administration, the reality is that over the longer-term presidents and parties have historically had very little impact on financial returns.

The large-cap US index has had double digit annualized total returns during every presidency, except one – that exception being George W Bush’s, which coincided with the dot-com bubble burst. Furthermore, that same index’s annualized returns were identical (16.3% per annum) during both Obama and Trump’s presidencies, despite their contrasting policies.

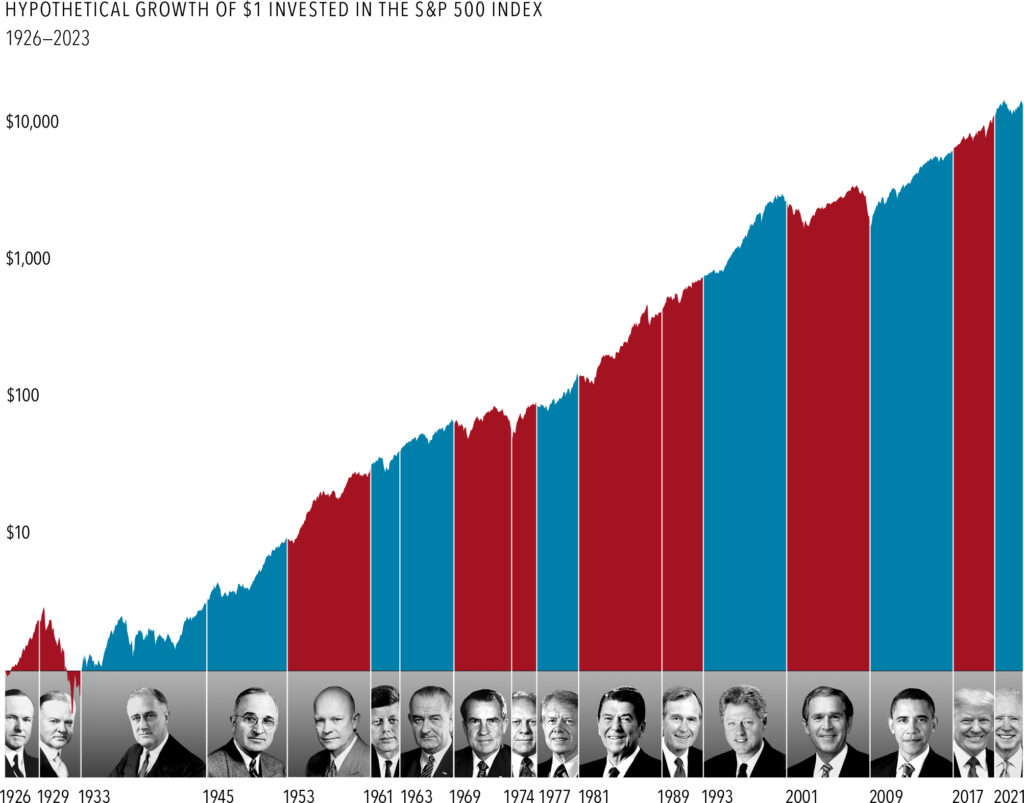

As a final reminder, as longer-term investors, it is important to recognise that ultimately it’s those (longer-term) fundamentals that matter more to markets than the outcome of elections, which the below graphic illustrates well.

Source: Dimensional, January 2024

Markets are unpredictable and volatile, particularly in the aftermath of such an important election – however, sticking to your financial goals and understanding the longer-term strategy has always proven to be the best course of action, regardless of whoever is in the White House.

For any queries, please speak to your financial adviser.

Charlie Buxton, Head of Investment Consulting

Please Note

The information contained in this document is for information purposes only and should not be construed as a solicitation, offer, or as a recommendation to acquire or dispose of any investment. The Progeny Group uses reasonable efforts to obtain information from sources which it believes to be reliable. However, The Progeny Group cannot guarantee that the information or opinions contained in this report are accurate, reliable or complete. The information and opinions contained in this update are subject to change without notice. The value of investments and the income from them can go down as well as up and past performance is not a guide to the future performance.