Autumn budget tax implications

With the general election behind us, we are now focusing our attention on the planned Budget, which is scheduled for 30 October 2024.

In an earlier piece, I wrote about how the various manifesto pledges from Labour might impact you. In both the pre-election period and since then, Chancellor Rachel Reeves has stated that she does not intend ‘to raise taxes on working people’. This means that we do not expect Income Tax, National Insurance, or VAT to increase. Similarly, Reeves has also stated in the News Agents podcast that taxes will need to increase, so this logically leads to the question of which taxes will have to rise.

Income Tax, National Insurance, and VAT generate around three-fifths of all tax revenue (£627 billion in 2023/24), so ring-fencing these from increases puts a lot of emphasis on other taxes to make up the difference.

There are a limited number of other taxes that are sufficiently large enough that increasing them would make a meaningful difference to the total tax take. Amongst these are Capital Gains Tax (CGT), Inheritance Tax (IHT), and pension tax relief.

Although other taxes could be altered, they are unlikely to make enough of a difference to the overall fiscal picture to be worthwhile. In this article I discuss more about the Autumn Budget tax implications and how these possible changes may impact you.

Capital Gains Tax

At the moment, anyone who sells an asset for a profit is charged tax on it at either 10% (for basic rate taxpayers), or 20% (for higher and additional rate taxpayers). There are also special rates for when someone disposes of property of 18% and 24%, respectively. There is an annual exemption of £3,000 per person, but this doesn’t make much of a difference if the profit from the disposal is more than a very modest amount.

The think tank the Institute for Public Policy Research (IPPR) has suggested that aligning CGT rates with Income Tax rates would raise an additional £12 billion a year. This would return us to the position that prevailed between 1988 and 2008, where capital gains were taxed at the same rates as income. This was originally introduced by former Conservative Chancellor Nigel Lawson, and then revoked by former Labour Chancellor Gordon Brown.

This would mean that the highest rate payable on capital gains would increase to 45%, and likely to impact anyone selling a buy-to-let property, significant quantities of shares or other taxable investments, or anyone selling a business once they had made full use of their Business Asset Disposal Relief, formerly known as Entrepreneur’s Relief.

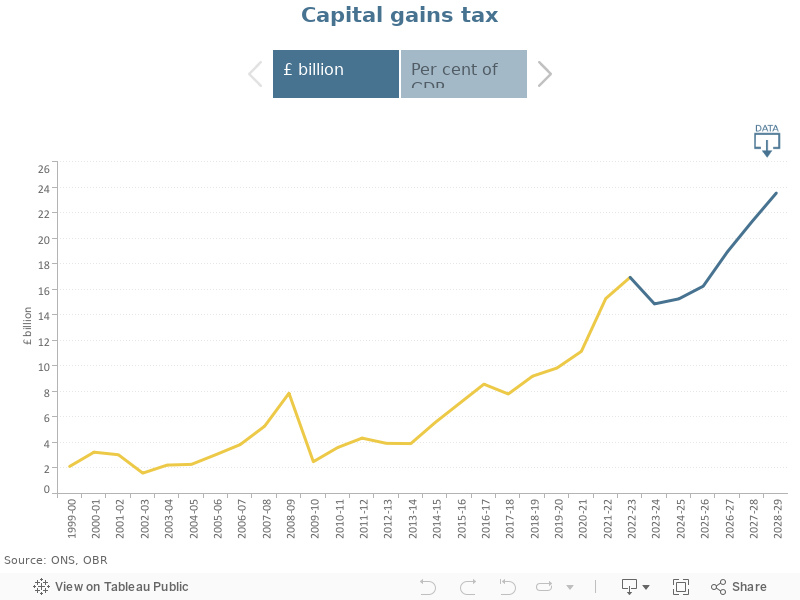

Leaving aside the potential reaction to this change, this would mean that capital gains and income would be taxed at the same rate for the first time in 16 years, which is a significant change. Even on present trends, CGT is expected by the Office of Budget Responsibility to raise around £24 billion a year by 2028/29, so whatever happens, this is big money.

Source: Office for Budget Responsibility – Recent trends and latest forecast

Inheritance Tax

Inheritance Tax (IHT) is levied on all assets that a person owns that are not exempt, and that are over the value of that person’s available allowances. Everyone is entitled to have up to £325,000 worth of value in their estate before paying the tax (£650,000 for a married couple), and there is also a further £175,000 per person (£350,000 for a married couple), where the family home is left to a child or grandchild. All assets above this level are taxed at 40%.

Whilst it does not seem likely that the headline rate of IHT will change, the exemptions are likely to remain frozen until 2028, meaning that they will not have increased since 2009. This means that an ever-increasing number of estates will become obliged to pay IHT as the average estate size increases, but the allowances remain unchanged.

There is also the possibility of reform to Business Relief and Agricultural Relief. These allow businesses and farmland to pass down to beneficiaries free of IHT. The Institute for Fiscal Studies has proposed this, and this all points towards IHT becoming a greater share of overall taxation as time passes.

Pension Tax Relief

Pension contributions that an individual makes personally (as opposed to being paid by their employer) benefit from tax relief at their marginal rate of income tax. In other words, if someone pays £10,000 into their pension from income that has been taxed at 40%, they get 40% income tax relief on the contribution. The net effect is to ensure that money placed into a pension has effectively entered the pension fund with no tax deducted. Income Tax is then levied when the money is later withdrawn and spent in retirement.

It is reported that the Chancellor is considering introducing a flat rate of pension tax relief for everyone at 30%. This would be a bonus for basic rate taxpayers who would normally only receive 20% relief, but would penalise higher and additional rate taxpayers who had previously received 40% or 45%.

When considering the Autumn Budget tax implications, this is a big area for reform, as pension tax relief results in £50 billion of tax rebates annually from the government to pension investors.

Autumn Budget tax implications – constructive reaction

Whilst there is not much that an individual can do to change the course of events set by the Chancellor, it is always possible to react to them in a constructive manner. Financial planning is at the heart of this and allows an investor to plan ahead with confidence. If you would like to discuss any of this with one of our financial planners, please get in touch.

As always, we will provide you with a comprehensive summary report of the Autumn Statement when it is announced in October.

Important Note

The information contained within this document is subject to the UK regulatory regime and is therefore primarily targeted at consumers based in the UK.

This article is distributed for educational purposes only. This communication does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs.

The opinions stated in this document are those of the author and do not necessarily represent the view of Progeny and should not be relied upon to make a financial decision.

Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Any links to third party websites provided are for convenience only. We do not control, endorse, or guarantee the content, accuracy, or availability of these external sites. Users access these links at their own risk.

Please note

Tax treatment depends upon individual circumstances and is based on current UK tax legislation, that is subject to change at any time.