In recent weeks, we have experienced a sharp U-turn in market optimism with the S&P500 20% below its January all-time high. The higher-than-expected CPI (consumer price index) report in the US, and subsequent interest rate rises have led to equity and bond prices falling.

Predictably enough, the financial media is full of apocalyptic headlines and instant emotional reactions. We, as investors, are only human and it can be natural to want to respond in some way to news of such a dramatic global market drop in such a short space of time. However, market tumbles may be scary, but they shouldn’t be surprising.

For long-term investors, reacting emotionally to down markets may be more detrimental to portfolio performance than the decline itself and can derail progress made toward reaching your financial goals. As an investment manager, it’s my job to agree on a strategy with financial planners and their clients and encourage them to stick to it when the waters get choppy.

Do downturns lead to down years?

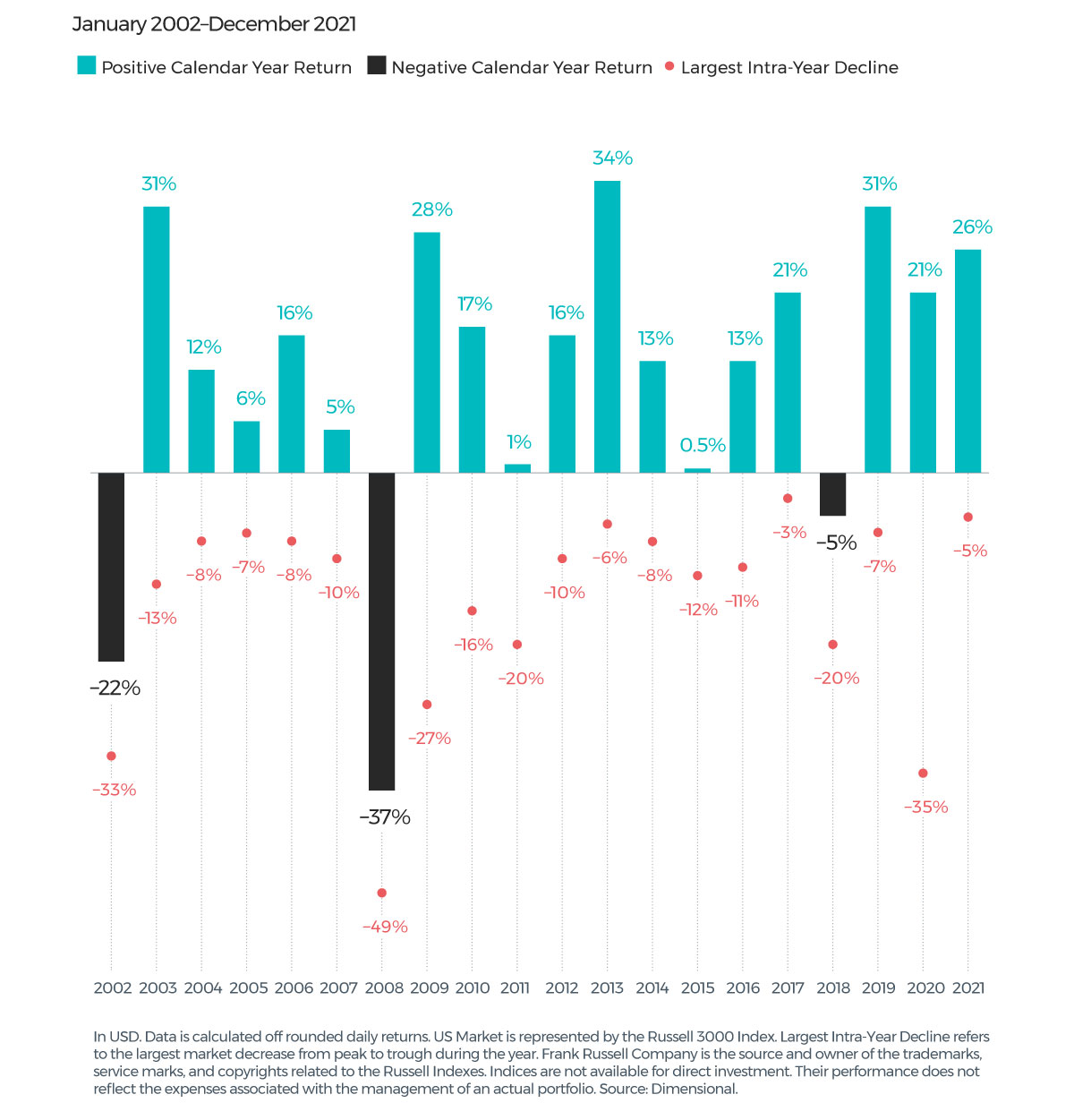

In times of turbulence, it can be helpful to look to the history books to provide some perspective. Stock market declines over a few days or months may lead investors to anticipate a down year. But the US stock market had positive returns in 17 of the past 20 calendar years, despite some notable dips in many of those years. The graph below shows the calendar year returns for the US stock market, since 2002.

The intra-year declines for the index ranged from 3% to 49%. Many years with large intra-year declines saw positive annual returns. Even in 2020, when there were sharp market declines associated with the coronavirus pandemic, US stocks ended the year with gains of 21%.

This shows both just how common market declines are and how difficult it is to say whether a large intra-year decline will result in negative returns over the entire year.

US market intra-year declines vs. calendar year returns 2002-2021

Reacting can hurt performance

Reacting can hurt performance

The reaction of some investors to volatility is to consider whether it’s possible to time their entry into the market to avoid the potential losses associated with periods of turbulence, with the aim of aiding the long-term performance of their portfolios. The answer to this is that it is unlikely that investors can successfully time the market, and in instances where it has been achieved, it may be a result of luck rather than skill.

It’s also worth noting that a substantial proportion of the total return of stocks over long periods of investing is derived from just a handful of days in those periods. As with predicting periods of turbulence, investors are unlikely to be able to identify in advance which days will have strong returns and which will not. Faced with this scenario, the prudent course of action is to remain invested during periods of volatility rather than jump in and out of stocks, otherwise an investor runs the risk of being on the side-lines on days when returns happen to be strongly positive.

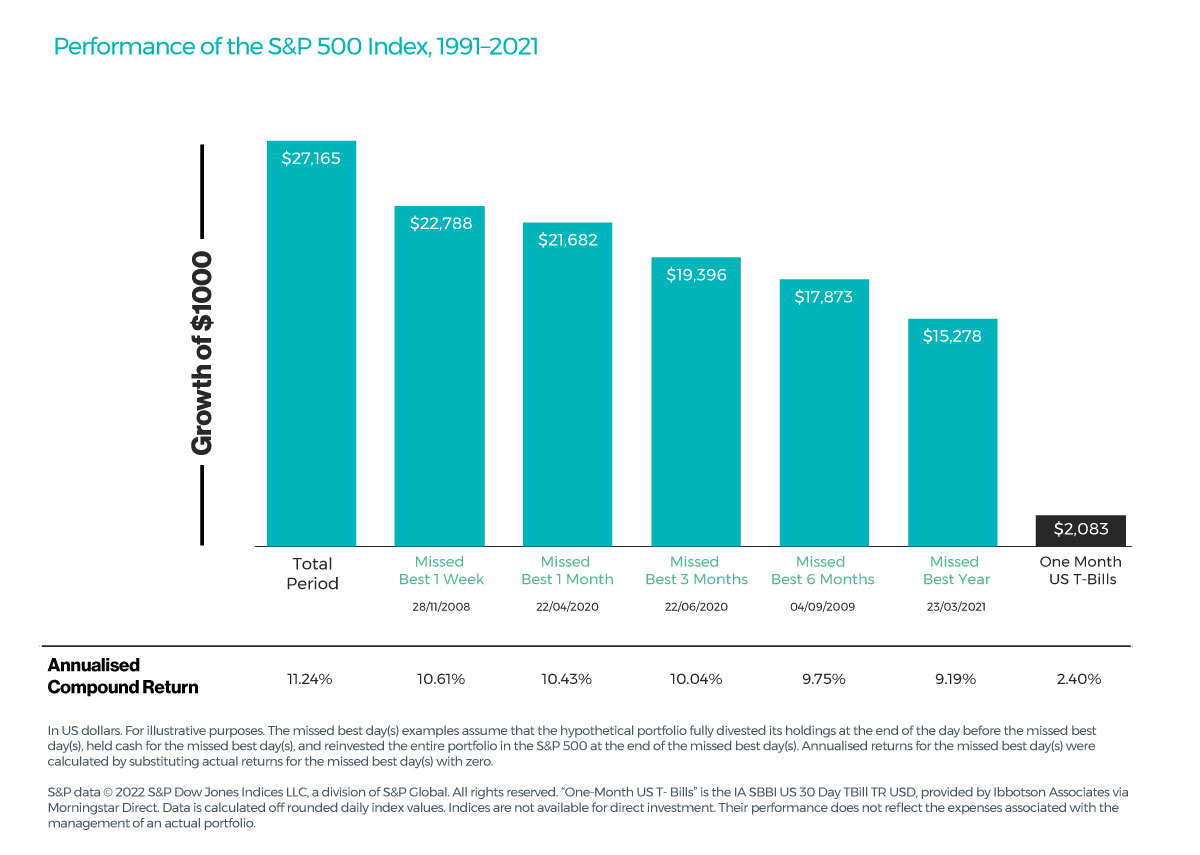

A further graph, below, helps to illustrate this point. It shows the annualised compound return of the S&P 500 Index going back to 1991 and illustrates the impact of missing out on just a few days of those strong returns. The bars represent the hypothetical growth of $1,000 over the period and show what would happen if you missed the best single day, or a handful of the best single days, during the period. The data shows that being on the side lines for only a few of the best single days in the market would have resulted in substantially lower returns than the total period had to offer.

Bull markets usually chase bear markets

Bull markets usually chase bear markets

While market volatility creates shockwaves and grabs the headlines, the other side of a bear market and worrying economic signals is an eventual bull market that has historically always materialised after such a sharp decline in stock prices. History shows the stock market tends to rebound quickly. The same can’t be said for individual stocks or even entire sectors which is a reason to remain broadly diversified.

As illustrated in the chart below, historically, on average, a year after the S&P 500 tipped into bear market territory (a 20% fall from the market’s previous peak), it rebounded by about 20%. And after five years, the S&P 500 averaged returns of over 70%.

Beyond a well-designed portfolio, one of the best ways to deal with periods of disappointing returns is to have planned for them. A financial adviser can help you develop a plan that factors in the chances you’ll experience some market lows and help you find the confidence to keep to your plan or ‘stick to the knitting’ as I would say.

Beyond a well-designed portfolio, one of the best ways to deal with periods of disappointing returns is to have planned for them. A financial adviser can help you develop a plan that factors in the chances you’ll experience some market lows and help you find the confidence to keep to your plan or ‘stick to the knitting’ as I would say.

If your plans have changed or you need advice on your investment management needs, please contact your financial planner, or contact us at Progeny and we’d be happy to discuss your circumstances.