A growing chorus of economists are predicting that the UK is heading for a recession. Economic growth has been slowing further and the outlook is that the UK will be among the weakest economies in the G7 nations next year.

Citi Group has predicted that inflation could peak at 18.6% in January 2023 which has further ratcheted up concern about the increasing cost of living.

The International Monetary Fund (IMF) has downgraded its UK growth forecast for 2022 to 3.2%, from 3.7% in April. This has already been downgraded from 4.7% at the start of the year.

The Consumer Prices Index (CPI) rose by 9.4% in the 12 months to June 2022, up from 9.1% in May. On a monthly basis, CPI rose by 0.8% in June 2022, compared with a rise of 0.5% in June 2021.

There have been calls for an ‘emergency Budget’ across the political divide, and it is likely that we will see a financial statement of some kind from the incoming Prime Minister as soon as mid-September.

At an international level, the IMF also warned that stalling growth across the world means it could be “teetering on the edge of a global recession”. Global inflation forecasts have worsened over the past quarter as the cost of living has been hit by rising food and energy prices.

If we do move into recession, many investors will be concerned as to what this means for markets and how this will affect their investments.

What is a recession?

To understand what a recession means for markets and investors, we need to first understand what a recession is.

A recession is defined simply as: two consecutive quarters of contraction in a country’s economy, signalled by a reduction in gross domestic product (GDP) and rising unemployment, among other factors. The end of a recession is marked by the point where the economy starts to grow beyond the original pre-recession position.

Every recession varies in terms of length, severity and consequences. They can happen in times of low or high inflation. The shocks hitting the economy and the policy response will influence the type of recession.

Sometimes bonds and shares fall at the same time, as we saw earlier this year. But this is not typical. Often they coincide with high unemployment however the United Kingdom is currently experiencing the lowest unemployment rate is since 1974 at 3.8% in June. In the US, it’s been a similar picture at 3.6%.

How are markets impacted?

A century of economic cycles has shown that we may well be in one before economists make that call. Markets tend to be efficient and one of the best predictors of the economy is the stock market itself. Markets tend to fall in advance of recessions and start climbing earlier than the economy does. Financial markets are quick to price in event, but economic data takes longer to come through.

Downturns in markets lead to cheaper share valuations in the short-term, however in the long-term this can bring higher expected returns. Higher interest rates should lead to increased valuations in the short-term for bonds that tapper in the long run.

A recession is not a reason to sell

Although recessions are a natural occurrence in our modern economy, they are unpredictable periods that can dominate headlines with gloom and significantly impact the mindset of investors.

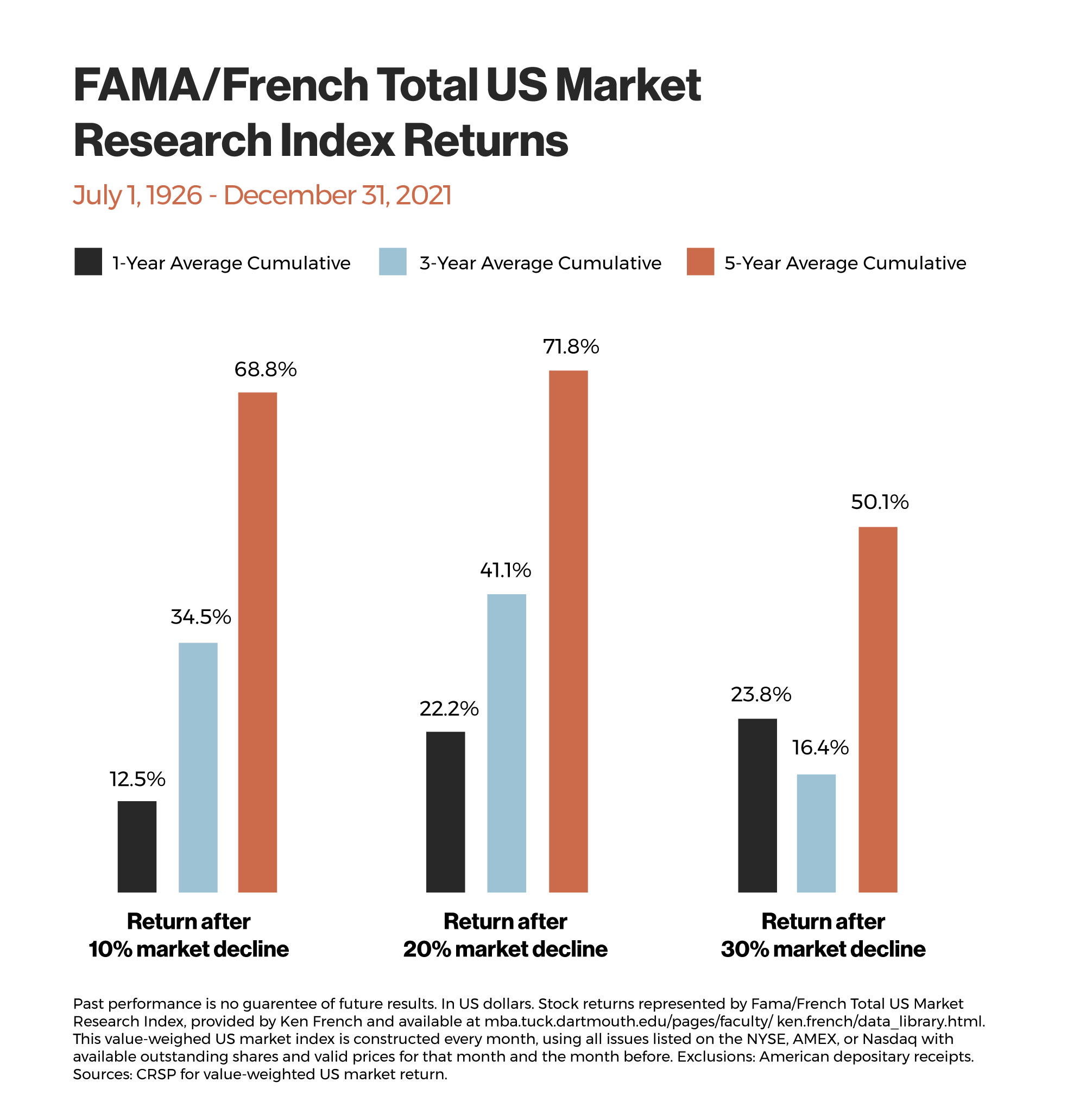

Whether accompanied by recessions or not, market downturns can be unsettling often resulting in investors overreacting until more information becomes available. However, markets around the world have often rewarded investors that don’t sell even when economic activity has slowed. This is partly because the best and worst trading days often happen close together.

Professional services like asset management are not so much about creating certainty – after all, that’s impossible when it comes to the future – but about reducing and managing uncertainty. We help to develop plans that factors in the chances you’ll experience some market lows and improve the journey.

This is what we do, we address uncertainty, take it off your hands, so you can live your life and concentrate on what matters to you.

*Source: Fama / French total US market research index returns July 1, 1926 – December 31, 2021