In 2016, the UK market reached new highs and stocks in a majority of developed and emerging market countries delivered positive returns. UK investors with overseas assets benefited from the decline of the value of the pound, with Sterling falling 16% against the US dollar.

The year began with anxiety over China’s stock market and economy, falling oil prices, concern about the impact of the strong yen on the Japanese economy and uncertainty around the impact of the UK’s EU referendum. Many world equity markets were in steep decline for the first few weeks of the year. In spite of this shaky start, many markets ended the year close to (or breaking) all-time highs.

Many investors may not have expected global stocks and bonds to deliver positive returns in such a tumultuous year. This turnaround story highlights the importance of diversifying across asset groups and regional markets, as well as staying disciplined despite uncertainty. Although not all asset classes had positive returns, a globally diversified, cap-weighted portfolio logged attractive returns in 2016.

Consider that global markets are incredible information-processing machines that incorporate news and expectations into prices. Investors are well served by staying the course with an asset allocation that reflects their needs, risk preferences and objectives. This can help investors weather uncertainty in all of its forms. The following quote by Eugene Fama describes this view.

“There is no information in the past three to five years. It’s just noise. You have to really decide what your strategy is based on—long periods of returns—and then stick to it.” — Eugene Fama

Returns from individual countries were typically varied. Among developed markets, Canada performed the best (+48.6%), while Israel performed worst (-10.3%). In emerging markets, Brazil performed the best (+98.2%) and Greece the worst (4.82%).1

Brazil is a noteworthy example of how difficult it is to predict market returns and time markets. The country is currently experiencing political and economic distress—the OECD predicted that its domestic output would contract 3.4% in 2016—yet its stock market returned 38.9% last year in local currency terms. Market prices incorporate, and thus represent, a rich set of information, including expectations about the future. In order to identify mispricing and beat the market, investors must challenge the market’s aggregate wisdom. Academic research suggests this is very difficult to do with consistent success.

Global equity markets have enjoyed strong returns since the financial crisis of 2008-09, and many times in the past few years, people have speculated about what might halt the rise of global equity markets. Several events occurred in 2016 that were suggested as potential catalysts for markets to decline. However, a globally diversified, cap-weighted portfolio delivered positive returns in 2016.

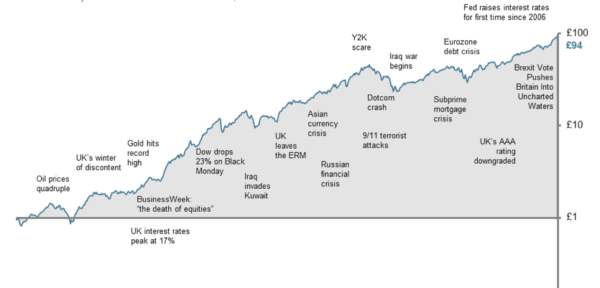

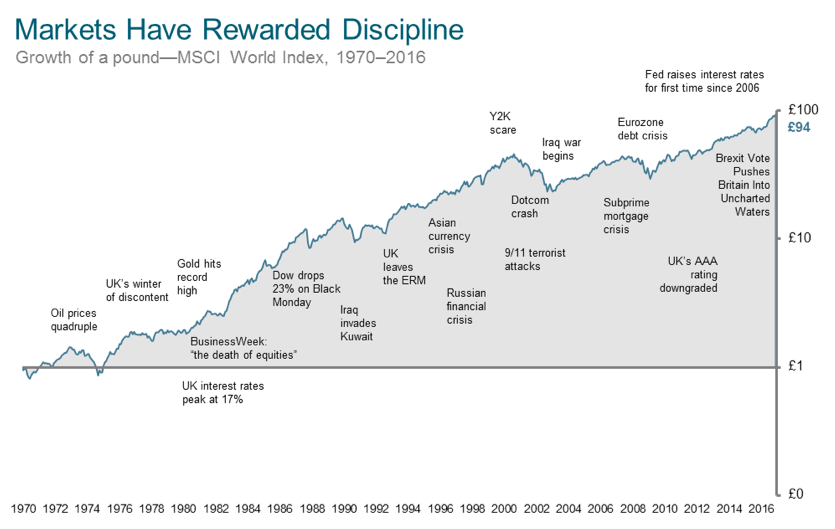

The chart above puts 2016’s return in a long-term context. It illustrates that investors have enjoyed positive long-term returns throughout the 1970s crisis, Black Monday, Black Wednesday, wars, currency crises, bubbles and crashes. 2016 adds to that list with Brexit and the US presidential elections. This shows that, rather than making investment decisions based on headline news, investors are better served by following a disciplined approach to investing, based on a long-term financial plan that reflects their individual needs, risk preferences and objectives.

“If three or five years of returns are going to change your mind [on an investment], you shouldn’t have been there to begin with.” — Eugene Fama

—

1 Source: MSCI data © MSCI 2017, all rights reserved. Returns expressed in GBP. Past performance is no guarantee of future results. Indices are not available for direct investment, therefore their performance does not reflect the expenses associated with the management of an actual fund.

This article does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs. Past performance is not a guide to future performance. The value of an investment and the income from it may go down as well as up and investors may not get back the amount originally invested. This document may include forward-looking statements that are based upon our current opinions, expectations and projections.