The Labour government’s first Spending Review was delivered against a political and economic backdrop that looked very different to the one following last July’s election.

HIGHLIGHTS

- No tax announcements, which will have to await the Autumn Budget.

- Capital spending to increase by £113 billion through to 2029/30.

- Overall day-to-day spending to rise by 1.2% a year in real terms over next three years.

- The NHS is a major winner, with a real day-to-day spending rise of 3%.

- Overall investment spending on defence up by 7.3% a year in real terms.

- By April 2027, defence spending (including intelligence) will stand at 2.6% of GDP.

- Long term investment funding commitments across transport infrastructure, social housing and prison places.

- The Home Office and Foreign, Commonwealth and Development Office are the major losers.

The political background

Spending Reviews may not attract the media attention of Budgets, but their impact is arguably more significant for the average voter. Whereas a Budget is all about raising revenue, the Spending Review sets out where and how the money is spent. Spending Reviews do not cover all government expenditure; their focus is on the more stable elements of departmental spending rather than on demand-led and less predictable costs, such as welfare. The latter account for slightly more than half of all government spending.

Traditionally Spending Reviews have had a timeframe of three years, giving departments a reasonable period over which to plan their finances. However, since 2013 the triennial cycle has been interrupted by election timing and the pandemic. The last three-year spending review took place under Rishi Sunak in autumn 2021, alongside the Budget, and covered the period 2022–2025. In the Spring 2024 Budget Jeremy Hunt announced that the next Spending Review would not take place until after the general election, then expected to be in autumn of that year.

The deferral was seen as motivated by the difficult spending decisions the government faced. At the time, the chair of the Office for Budget Responsibility, Richard Hughes, was on record as describing the Chancellor’s spending plans beyond 2025 as “worse than fiction”, so lacking were they in detail. When Rachel Reeves entered 11 Downing Street in July 2024 it was initially unclear whether she would produce a 2025–28 spending review to accompany her autumn Budget. In the event, by November 2024 she had decided to defer the full review and use the departmental spending limits for 2025/26 set in the Budget.

The delay allowed the Chancellor to make the spending review ‘zero-based’, meaning that in theory departmental budgets were set from zero, with all spending assessed on value for money, rather than working from existing budgets and deciding increases or decreases. This ground floor approach was last seen in George Osborne’s 2010 review.

The new review covers day-to-day spending for three years (to 2028/29) and capital expenditure for four years (to 2029/30). However, following the House of Commons’ approval of the most recent Charter for Budget Responsibility in January 2025, subsequent Spending Reviews will now take place every two calendar years, and will set spending limits for government departments for at least three years. As a result, the figures in the latest Spending Review for the period beyond 2027/28 should be treated with caution as they will overlap with the next review and coincide with the likely run-up to the next general election.

The economic and fiscal background

In the autumn 2024 Budget the Chancellor announced two new fiscal rules, both designed to give greater scope for borrowing to finance capital investment:

- The stability rule, which Reeves defined as the fiscal mandate. At present this rule requires the current budget (day-to-day expenditure less revenues) to be in surplus by 2029/30. In 2024/25 the current budget is estimated to have been £70.3 billion in deficit, £8.4 billion up on 2023/24. The Office for Budget Responsibility’s (OBR’s) latest (March 2025) projections are that:

- the current budget will be in surplus by £9.9 billion in 2029/30 (the widely quoted ‘headroom’ figure) and

- the probability of the rule being met is 54%.

- The investment rule, also known as the supplementary target. This rule currently says that public sector net financial liabilities (PSNFL) must be falling as a proportion of gross domestic product (GDP) by 2029/30. Between 2023/24 and 2024/25 PSNFL are estimated to have risen by 3.3% to 83.5% of GDP. The OBR’s latest projections for this target are:

- PSNFL will fall by £15.1 billion (0.4% GDP) between 2028/29 and 2029/30 and

- the probability of the rule being met is 51%, “based on historic forecast errors”.

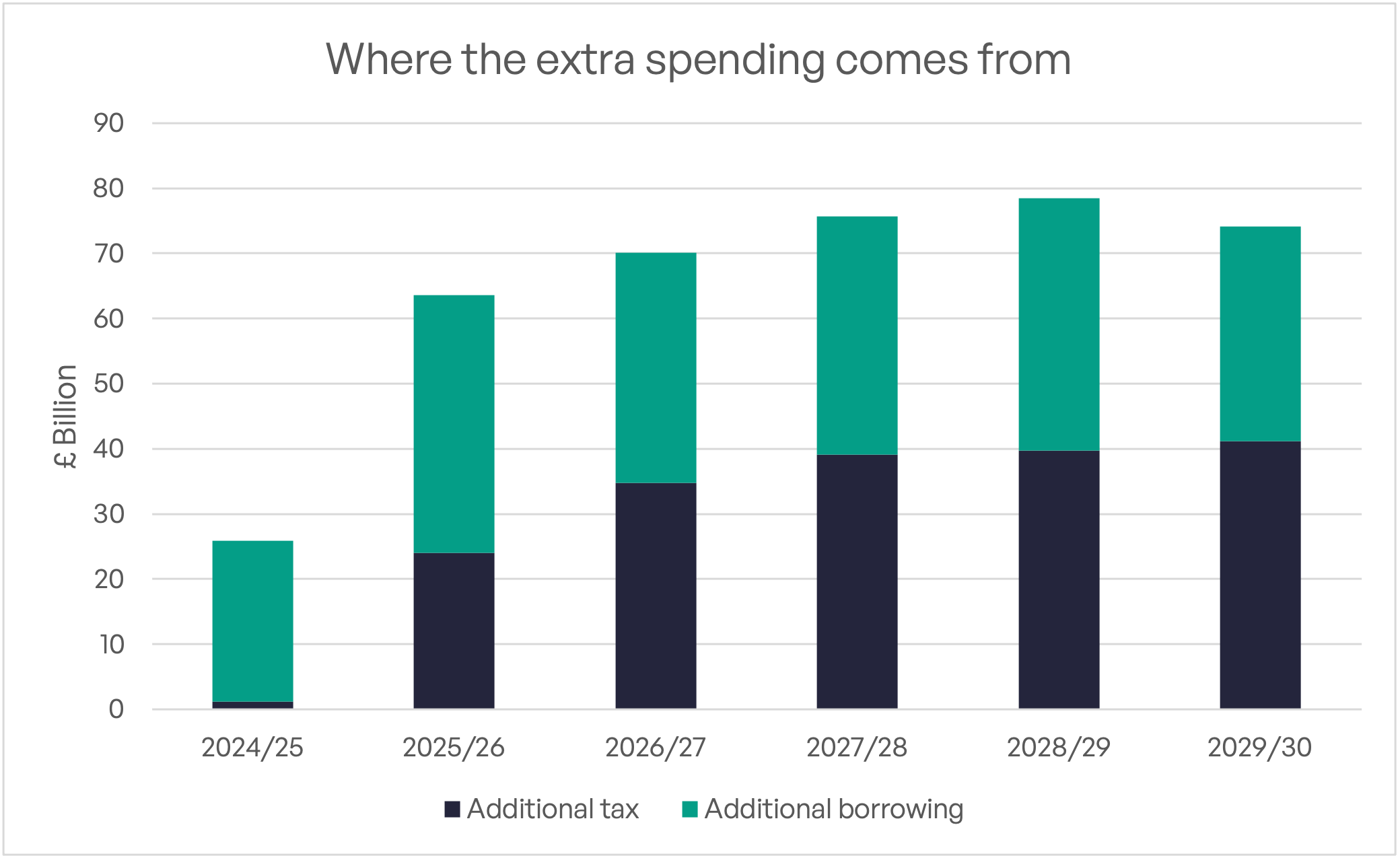

In addition to increased scope for borrowing, Rachel Reeves also raised taxes in her first Budget, with an extra £41 billion flowing into the Treasury in 2029/30. The overall result was that the autumn 2024 Budget projected a total increase in all government spending over the four years from 2026/27 of almost £300 billion, split about 50/50 between higher borrowing and increased tax revenue.

Source: HM Treasury October 2024

One notable aspect of the autumn 2024 Budget projections was that the rise in spending was loaded towards 2024/25 and 2025/26, after which spending growth slows markedly, as demonstrated in the graph above. Based on Budget data, the Institute for Fiscal Studies (IFS) estimates that in real terms day-to-day expenditure was planned to grow by an average of 1.2% each year between 2026/27 and 2028/29, a figure confirmed in the papers issued alongside the Spending Review.

This relatively modest number starts to look much smaller for those departments that do not fall into the ‘protected’ category (such as defence and the NHS) which have traditionally received higher than average increases. Ahead of 11 June, the IFS, among others, was expecting to see some departments suffer real terms cuts, which proved to be the case. For example, the Home Office will see real day-to-day expenditure cuts of 1.7% a year and Transport 5% a year. In total eight departments face day-to-day real terms spending cuts. This may not be immediately apparent as in some instances the government has used cash-based figures or quoted real growth figures covering a period of five or six years rather than three or four.

THE CHANCELLOR’S STATEMENT

In a highly political speech, the Chancellor emphasised the areas where she was increasing both day-to-day and/or investment expenditure, while playing down those which were not so generously treated.

Defence

A predictable ‘winner’ was the Ministry of Defence, which the Treasury says will see a real terms spending increase of £11 billion. This is heavily weighted to investment, which has a real terms growth of 7.3% a year over the four years to 2029/30. The investment focus is on a sovereign nuclear warhead programme, infrastructure funding to renew military accommodation and building new munitions factories.

Day-to-day spending on defence grows much less quickly in the period to 2028/29 – just 0.7% a year in real terms. The bias towards investment has the advantage of falling outside the fiscal mandate rule. In contrast, spending under the aid budget, which was cut to allow for the defence expenditure rise, was largely day-to-day spending. The Chancellor said that by April 2027 overall defence spending (including intelligence) would be 2.6% of GDP.

The NHS

The Department for Health and Social Care (DHSC which covers the NHS) was also a beneficiary of the Spending Review. It will receive a real terms increase of 2.8% a year in day-to-day spending over three years, which translates into 3.0% for NHS England alone. However, that growth rate is slower than the long term average of around 3.5% a year. By 2028/29, the day-to-day DHSC expenditure (excluding depreciation) will be £232.0 billion, nearly 41% of the regular spending covered by the Review.

On the investment front, the news is not as good: the DHSC will see flat real terms growth over four years to 2029/30, as investment growth has been concentrated in 2024–26.

Education

Education will have a 0.7% a year real terms increase for day-to-day expenditure, which translates into 0.4% a year for the core schools’ element. Overall investment will rise slightly faster, at 1.3% a year. Reeves confirmed the extension of free school meals to all children with a parent receiving Universal Credit at a cost of £410 million a year by 2028/29.

Justice

The Department of Justice will enjoy 1.8% real terms growth in day-to-day expenditure, but its investment expenditure will suffer a real terms cut of 2.1% a year.

Energy

Day-to-day expenditure at the Department of Energy Security and Net Zero will rise by 0.5% a year in real terms, a slower pace than in 2024–26. Investment, including funding for home-grown clean power and carbon capture, will grow by 2.6% a year, again a reduced rate compared to 2024–26.

Local government and housing

Local government core day-to-day spending power will increase by 2.6% a year, thanks to an extra £3.4 billion of grant funding in 2028/29 over the 2024/25 figure. The Chancellor also confirmed £39 billion for a new Affordable Housing Programme, although the ten-year timeframe for this extends beyond the end of the next Parliament.

Home Office

Of the larger spending departments, the biggest loser was the Home Office – the last department to settle according to media reports. Day-to-day spending is set to fall by 1.7% a year in real terms, although this is not as fast as the drop in 2024–26. The picture for police core spending power (which includes local council precepts) is rosier, with real terms increases of 1.7% a year.

Foreign Office

The Foreign, Commonwealth and Development Office (FCDO) is the hardest hit department, albeit a small one, with real day-to-day spending cuts of 6.9% a year. The FCDO will see its investment also suffer real terms cuts of close to 7% a year.

Transport

Transport, a similarly sized department to the FCDO in terms of day-to-day spending, will suffer real terms cuts of 5% a year. However, it will benefit from 3.9% a year real growth in investment in the four years to 2029/30 (excluding HS2). Funding of £15.6 billion by 2031/32 was announced for local transport in England’s city regions, with additional investment across other projects including railway infrastructure.

Devolved nations

The devolved nations will receive corresponding increases to their settlements under the Barnett formula. The Treasury Spending Review press release makes a point of stating the extra amounts per head for Scotland, Wales and Northern Ireland over spending in England – 20%, 20% and 24%.

CONCLUSION

After considerable trailing, the Spending Review proved to be much as expected, with the NHS and Defence to the fore and the Home Office and FCDO to the rear. There are still important documents relating to the Spending Review to appear, notably the much-deferred Industrial Strategy and the ten-year infrastructure plan.

Once the missing documents are published – probably later this month – the Chancellor’s focus will turn to her autumn Budget, the date of which was not announced alongside the Spending Review. Having spelled out a raft of spending and investment commitments, she will be hoping that the OBR does not force her to raise taxes and/or borrow more as a result of the revisions it will inevitably make in the autumn 2025 ‘Economic and Fiscal Outlook’.

Important Note

The information contained within this document is subject to the UK regulatory regime and is therefore primarily targeted at consumers based in the UK.

This article is distributed for educational purposes only. This communication does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs.

The opinions stated in this document are those of the author and do not necessarily represent the view of Progeny and should not be relied upon to make a financial decision.

Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Please note

Tax treatment depends upon individual circumstances and is based on current UK tax legislation, that is subject to change at any time.

Past performance is no guarantee of future performance.

The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Your capital is therefore always at risk. It should be noted that stock market investing is intended for the longer term.