The old adage “if you fail to plan, you are planning to fail” is as relevant today as ever and, despite the unpredictability of investing, is the key to long-term financial security. While the Chancellor’s latest announcements on pension rules may have ignited political debate about whether retirees will opt for the instant gratification of a Lamborghini, the more important message for all of us should be about getting our financial plans organised. Much media coverage and anecdotal comment would suggest that few have considered retirement in detail, perhaps relying more on wishful thinking, rather than evaluating the many financial planning “what ifs”.

Given that financial peace of mind requires enough after-tax income to at least match expenditure in the long-term, it’s surprising that many of us tend to focus mainly on short-term cashflow. Major decisions about work, property, supporting others or making investments should be made with an understanding of how these may impact future wealth and security.

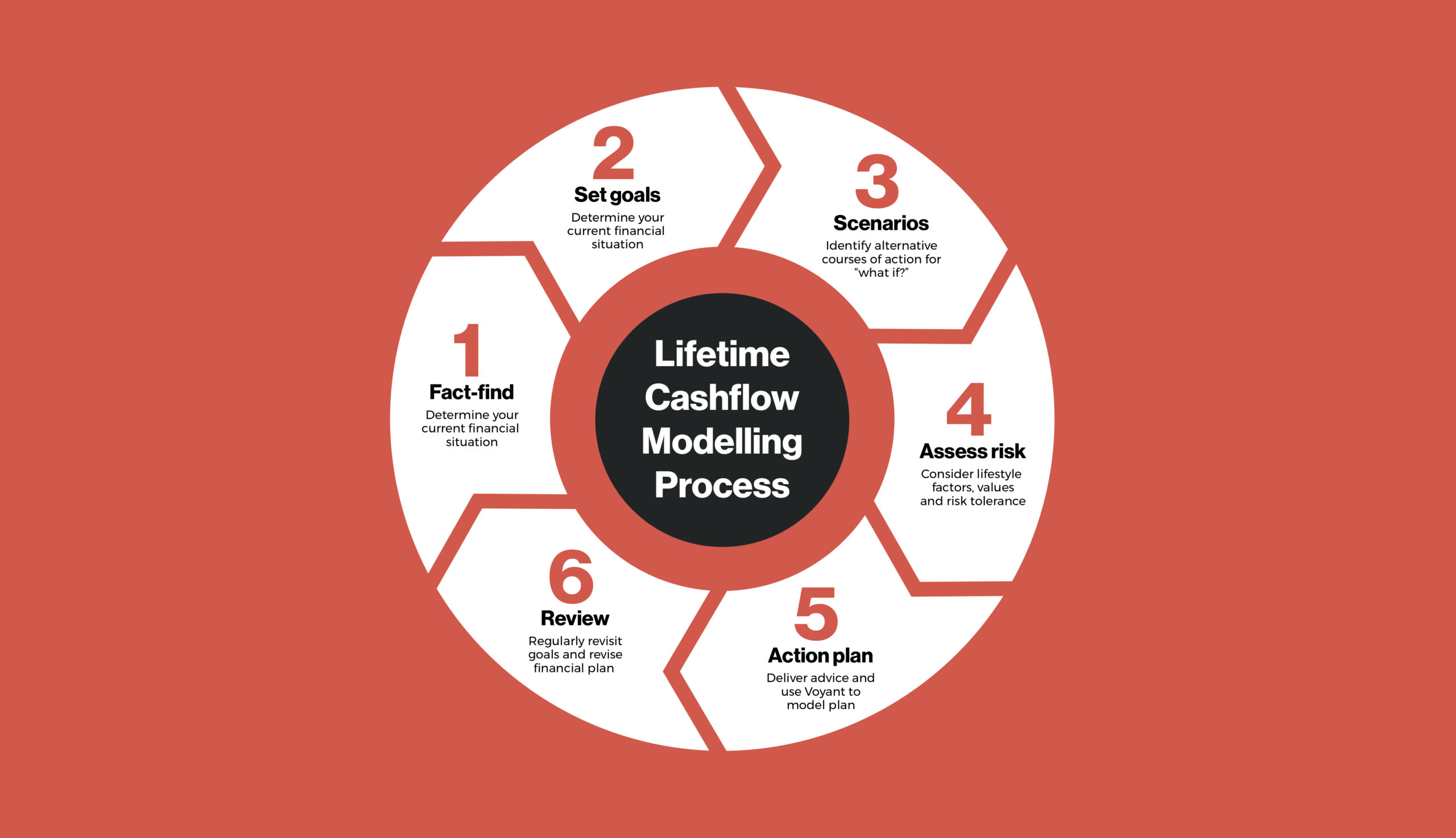

We use a process called ‘Lifetime Cashflow Modelling’ to help clients plan for the future. Lifetime Cashflow Modelling is aimed at individuals who wish to become (and remain) financially well organised. By illustrating the effects of pretty much any financial action or change, at any point in time, our advisers are able to help clients plan ahead for life’s changes and opportunities, whilst considering questions such as:

- When can I afford to retire, and could I consider partial retirement?

- If I want to provide financial support to loved ones, will I still be able to live comfortably?

- What rate of investment return do I need, to achieve my objectives?

- What level of financial risk should I be taking?

- Will downsizing my home in the future release enough cash to supplement my retirement? Do I have to downsize if I don’t want to?

- How will an inheritance tax bill impact my Estate? Are there ways of reducing this liability? What are the implications?

- If I die or get seriously ill, what will be the financial outlook for my family?

How does Lifetime Cashflow Modelling work?

The graphic below summarises 6-step the Lifetime Cashflow Modelling cycle:

Although the initial fact-find can seem a fairly lengthy process, the more detail, the more accurate the forecast will be. Your adviser will do most of the work before meeting, based upon the information supplied and their assessment of your wealth position. It is important to evaluate your lifestyle, write your “bucket list” and consider your values, responsibilities and aspirations, as well considering your current financial situation, in order to set out your long-term goals. All these factors are essential to the formulation of an action plan that can meet your objectives.

Planning for different factors and events that may influence your life is critical to the process. These identify alternative courses of action, which in turn leads to the assessment of risk tolerance. This is all taken into account and an action plan is produced to meet your current goals.

Once the information has been compiled and entered for the first time into our software system it is then a relatively simple process to keep your details up to date. The effects of inflation and the growth of investments are factored in, as are lifestyle changes.

Review and evolve plans

For any number of reasons, no plan stays perfectly on the course originally designed. So it’s important that you review your plan periodically, considering any adjustments that need to be made whilst keeping your sights set on your intended goals.

The frequency of review and any significant changes, needs to be carefully managed. Too many short-term adjustments may cause the plan to go from one extreme to another. Too few adjustments and the plan will be out of date. The aim is to follow an investment journey in keeping with the volatility anticipated and the level of risk of the solutions selected.

Just like the business plan of an organisation, lifetime cashflow modelling is of no value if the resulting financial plan is subsequently ignored or filed away!

We use Lifetime Cashflow Modelling and encourage our clients to review their financial plans annually. As part of our “Stewardship” process, we meet with them to discuss how their plan should be updated to suit their situations and goals. To learn more about how we could help you plan for the future, get in touch with us today or request a callback. We’d love to speak with you.

—

This article does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs. Past performance is not a guide to future performance. The value of an investment and the income from it may go down as well as up and investors may not get back the amount originally invested. This document may include forward-looking statements that are based upon our current opinions, expectations and projections.