It is always tempting to judge the value of your adviser on the recent performance of your investment portfolio. That is unfair as it fails to understand both the true value that a good adviser delivers with respect to investments and the fact that no manager can control the returns that the market delivers. A good adviser can earn their ongoing annual fee several times over, simply by helping clients to have patience, fortitude and discipline in their investing. As the founder of Vanguard and legendary US investor, John Bogle points out:

“If I have learned anything from my 52 years in this marvellous field, it is that, for a given individual or institution, the emotions of investing have destroyed far more potential investment returns than the economics of investing have ever dreamed of destroying.”

When it comes to investing, there are five key areas that your adviser provides significant value:

- Structure: The starting and critical step is getting your portfolio structure right for you. This must be based on your emotional and financial tolerance for, and need to take, risk. It involves selecting sensible risks to take and using high quality, low cost funds to capture the rewards that your earn for doing so.

- Governance: Making sure that your portfolio strategy and the funds that you own continue to deliver you with the greatest chance of a successful outcome and that you avoid fads and too-good-to-be-true products is important, yet much of this is behind the scenes and you may not see the work being done on your behalf.

- Hand-holding: The hardest part of investing is having the confidence and emotional fortitude to stick with the programme through thick and thin. When markets are either going up or down with great magnitude, as they inevitably do from time to time, an investor’s emotions will kick in either in the form of greed or fear often resulting in the destruction of wealth through a ‘buy high, sell low’ strategy.

- Rebalancing: Over time, portfolios drift in terms of their structure due to market movements resulting in either too much risk (equities have increased as part of the portfolio) or too little risk. Rebalancing seeks to ensure that the risk level of the portfolio remains where it was specifically designed to be. It takes stomach and discipline on behalf of your adviser to do this.

- Doing the boring stuff: The fifth level of value that an adviser delivers is undertaking some of the menial, yet highly valuable, administrative functions such as ensuring that ISA allocations are made use of and that capital gains are taken in a controlled manner, avoiding as little time out of the market as possible. We all hate paperwork, so let someone else take care of it!

Buy-high, sell-low strategy – favoured by many investors!

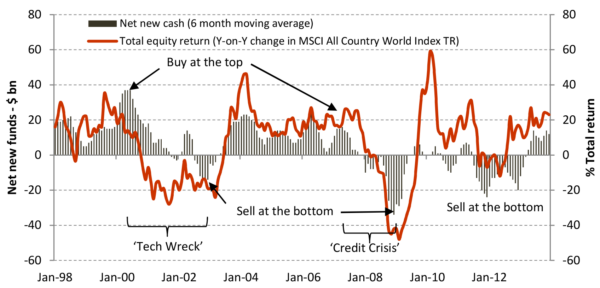

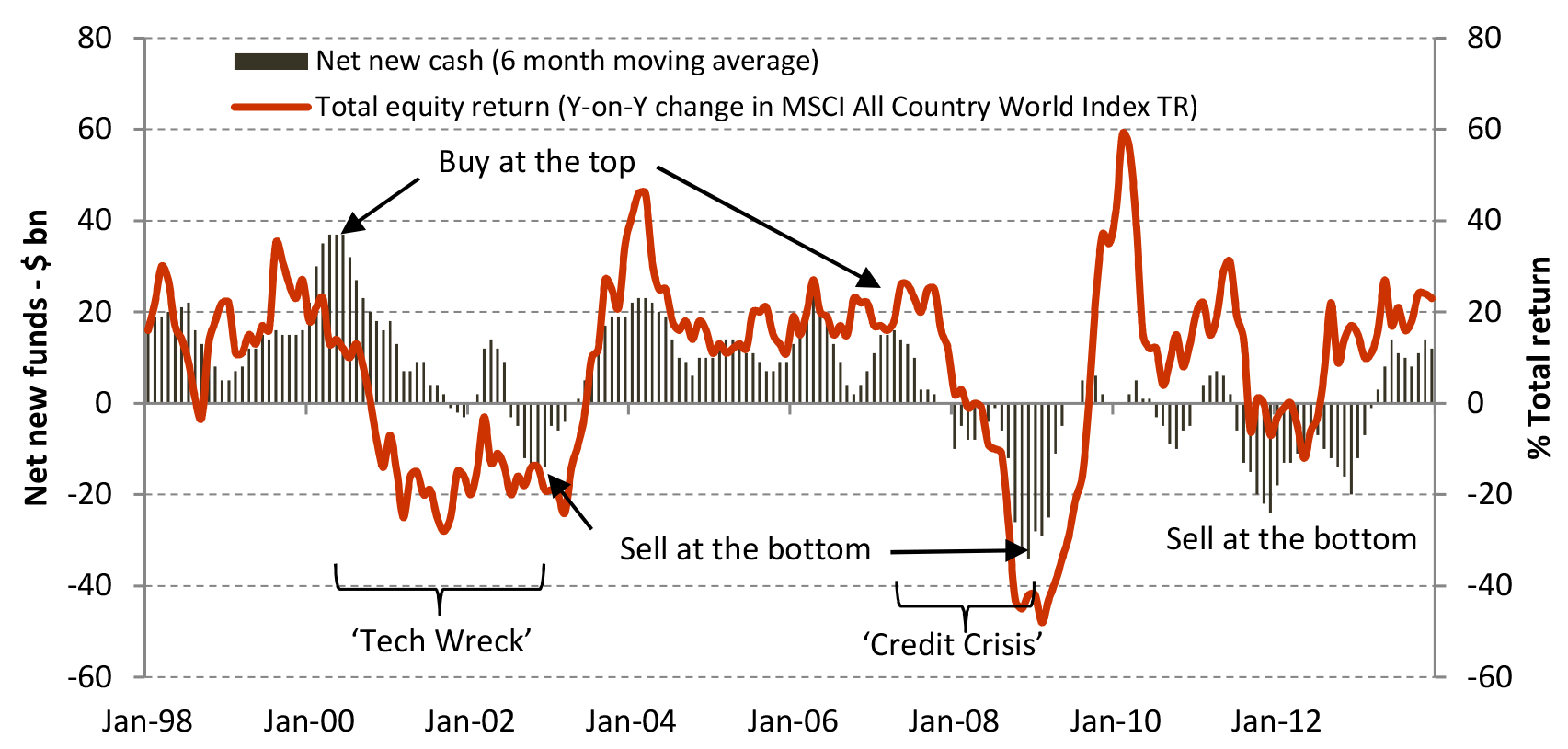

As an example of the hand-holding role of an advisor, take a look at the eye-opening chart below, which compares the flow of money into and out of equity mutual funds in the US to the year-on-year performance of the global equity markets. Investors load up on equities at the top of the market and sell when the markets crash, time and time again. The largest ever inflows into equity funds occurred almost exactly at the top of the tech boom in early 2000. The biggest outflows occurred at the lowest point of both the ‘Tech Wreck’ and the ‘Credit Crisis.’ In short, positive market returns result in investors buying equities and negative market returns result in investors selling equities!

Research by Morningstar reveals that the average difference on an annual basis between the returns of a fund and those that the average investor receives is -2.5% per annum to the detriment of investors, on account of their poor entry and exit timing. Given that most advisors charge 1% as an ongoing fee, which should also include comprehensive financial planning and regular goal tracking, it is easy to see the value of employing a steady hand to guide an investor through choppy waters.

In conclusion

So next time you look at a portfolio valuation, spare a little time to consider the broader, longer-term role your adviser is playing. What you are looking at is market noise, which risks tempting you into bad, emotional choices. Your adviser is there to provide perspective, stop you from owning investments that should be avoided, help you to keep faith in the programme and make you rebalance, just when you don’t want to! That’s what they are paid to do.

—

This post is a condensed form of our bi-monthly newsletter. To read the newsletter in full please click here.

This article does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs. Past performance is not a guide to future performance. The value of an investment and the income from it may go down as well as up and investors may not get back the amount originally invested. This document may include forward-looking statements that are based upon our current opinions, expectations and projections.