Inheritance tax receipts reached a record high in the 2022/23 tax year. With that in mind, is now a good time to assess the entire value of your estate?

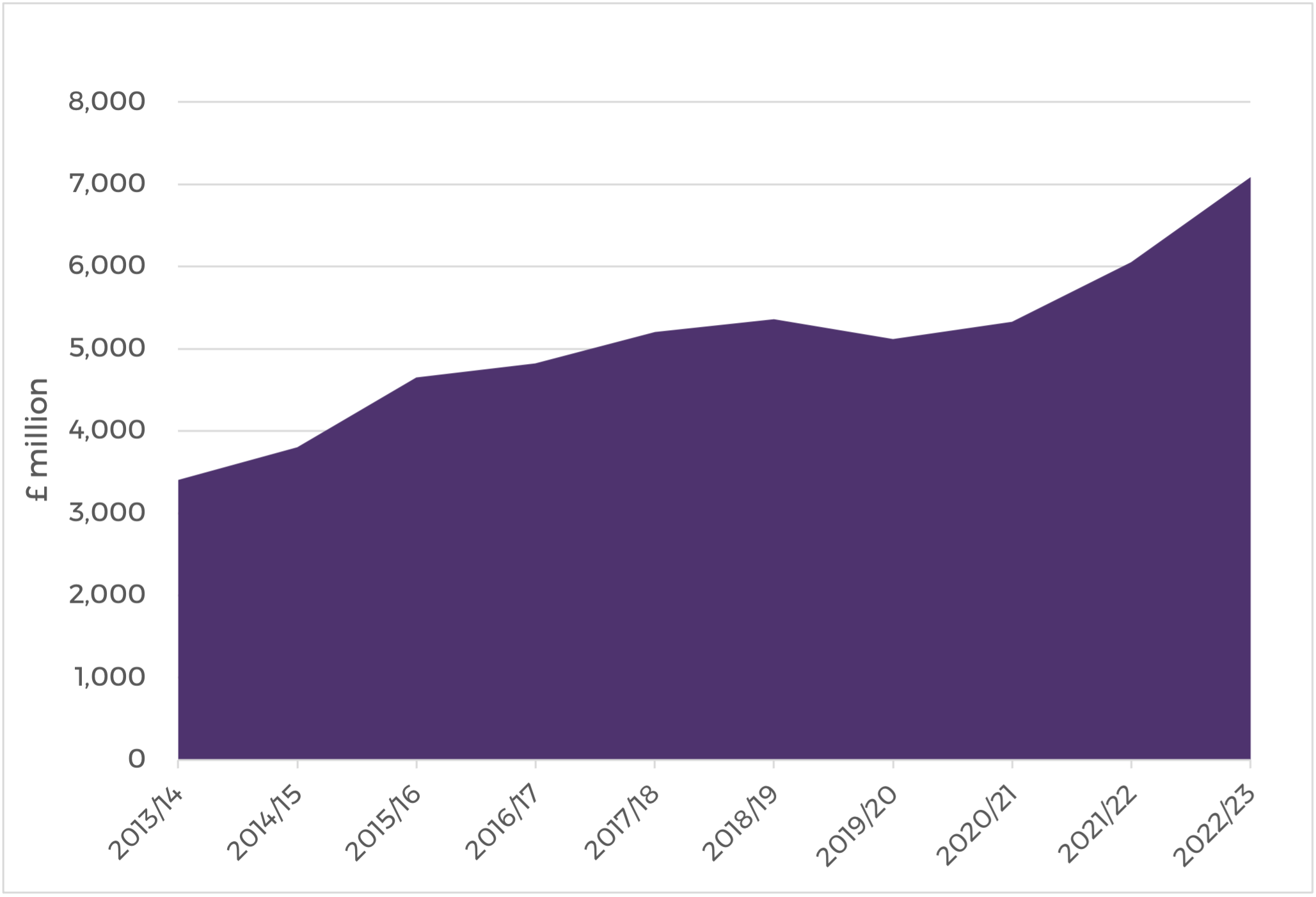

The government publishes monthly data that details HMRC’s cash tax receipts. The information shared in late April showed the first set of figures for the amount of £7.1bn raised in 2022/23. Between 2013/14 and 2022/23 there had been a 59.6% increase in overall HMRC receipts, and inheritance tax jumped by a whopping 108.3%.

The graph below shows that the steepest rise in IHT receipts happened in recent years. This could be due to the end of the residence nil rate band phasing (RNRB) and the rise in inflation.

Source: HMRC tax receipts and National Insurance contributions for the UK.

It seems as though the rise in inheritance tax receipts didn’t stop in the tax year 2022/23. According to Professional Adviser, HM Treasury collected £1.2bn in IHT in the first eight weeks of this tax year 2023/24. This was a 13% increase on what it had collected at the equivalent point in the last financial year. We also seem to be on track to break records again, as the ONS forecasts that IHT will raise £7.2bn by March 2024.

Inflation will play a significant role in rising IHT receipts, along with the nil rate band and RNRB which both remain frozen at their current levels (£325,000 and £175,000) until at least April 2028. Having a prolonged freeze during a time of high inflation can cause a ‘stealth’ tax increase. This pulls more estates into the IHT bracket and raises additional tax from those already caught in the catchment.

With this in mind, it may be a good time to re-evaluate your current estate plan and look at ways to mitigate the impact of IHT.

Structuring a will

As inheritance tax is paid out of your estate, one of the key ways of mitigating it is through your will. It’s important to have an accurate and up-to-date will in place to help ensure as much of your wealth as possible passes onto your chosen beneficiaries, rather than to HMRC.

Lifetime trust-based arrangements

Unlike wills, which only take effect after your death, a lifetime trust allows you to transfer the ownership of your assets to a trust while you are alive. These assets become the property of a lifetime trust. They will not be considered part of your estate, and you can leave these as gifts for your beneficiaries.

Taking advice from a legal and financial professionals can help you to navigate inheritance tax and help to mitigate the impact it may have on your estate. Contact our team today and we can help you to structure your will or lifetime trust.

Important Note

The information contained within this document is subject to the UK regulatory regime and is therefore primarily targeted at consumers based in the UK.

This article is distributed for educational purposes only. This communication does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs.

The opinions stated in this document are those of the author and do not necessarily represent the view of Progeny and should not be relied upon to make a financial decision.

Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Any links to third party websites provided are for convenience only. We do not control, endorse, or guarantee the content, accuracy, or availability of these external sites. Users access these links at their own risk.

Please note

Tax treatment depends upon individual circumstances and is based on current UK tax legislation, that is subject to change at any time.

The Financial Conduct Authority does not regulate will writing and some forms of estate planning.