My colleagues and I at Quadrant Group are fortunate enough to work with a diverse range of clients including entrepreneurs, professionals, architects, directors, artists, musicians and many more.

We help our clients with many complex financial issues along the way, whether they are accumulating wealth for the future or drawing an income in retirement. What they all have in common is that we start with the most basic concept of budgeting, or ‘balancing the books’.

This is not necessarily to cut costs or reduce outgoings. It’s about being in control over where money is being spent or saved. Whilst listening to discussions in the run up to the March 16th Budget, it seemed that all the talk was about how there was a need to ‘save 50p in every £100′ to balance the country’s books.

This got me wondering ‘can I save 50p in every £100’? How easy is this for an individual to actually do? If I could make that saving, what would it equate to? I decided to look at an example, based on an average income of £2,000 per month over a 20 year period, saving from between 50p to £20 of every £100 earned:

| Income Per Month | Saving per £100 earned | Time Period | Total Saved |

|---|---|---|---|

| £2000 | £0.50 | 20 years | £2400 |

| £2000 | £2.00 | 20 years | £9600 |

| £2000 | £5.00 | 20 years | £24,000 |

| £2000 | £10.00 | 20 years | £48,000 |

| £2000 | £20.00 | 20 years | £96,000 |

Seeing the results made me realise the impact that saving a relatively small amount can have over a long period of time.

Conversely, it shows the impact of NOT saving small amounts over the long term and the difference this can make to your plans and life!

When we build financial plans for our clients we look in detail at Cash Flow Planning. It is important to really understand your current and expected future income and outgoings, to enable us to realistically quantify what is needed to have a financially comfortable future. When did you last look at a detailed budget plan?

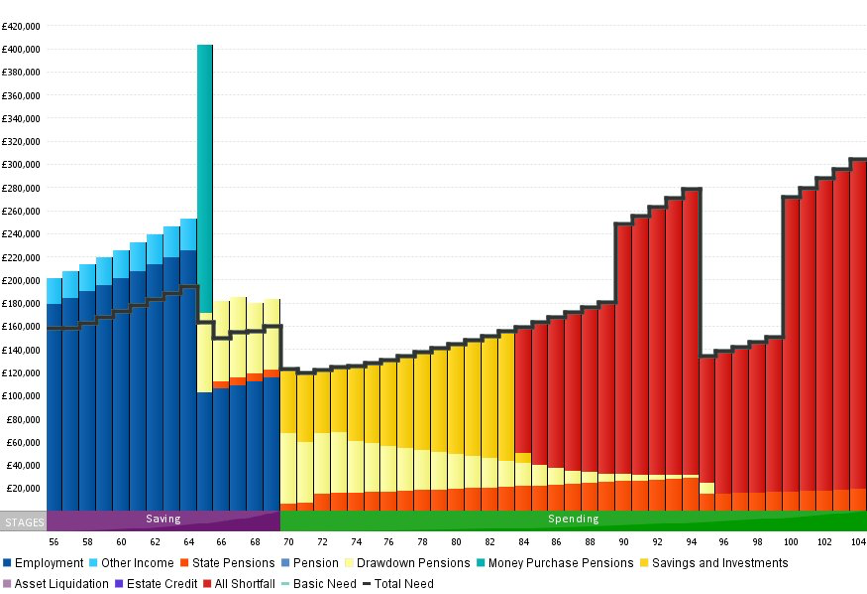

Example of Cash Flow WITH Surplus Income Invested – funds run out at age 84. Plan created using Voyant.

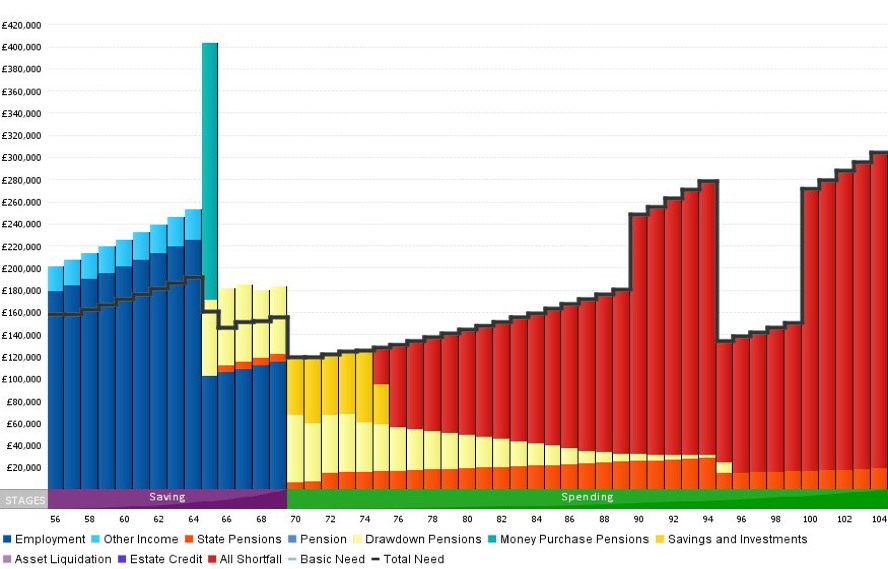

Example of Cash Flow WITHOUT Surplus Income Invested – funds run out at age 75. Plan created using Voyant.

When we look at surplus income or income after regular outgoings; how much of it do we really save? Or do we end up frittering away the £20 in every £100 that we could be saving?

An old adage in finance is ‘pay yourself first‘. My parents would certainly stand by this saying! It simply means: before you pay your bills, buy provisions, go out with friends, put money into savings. The first bill you pay each month should be yourself!

To take this further, what happens if the £2,000 monthly income stops? We ensure you have existing savings or income protection in place to ensure if you are off sick and unable to work you can still meet regular outgoings.

For every 50p in £100 you save by using tax efficient savings vehicles, drawing pension income tax efficiently, or inheritance planning over the years, it all adds up!

—

This article does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs. Past performance is not a guide to future performance. The value of an investment and the income from it may go down as well as up and investors may not get back the amount originally invested. This document may include forward-looking statements that are based upon our current opinions, expectations and projections.